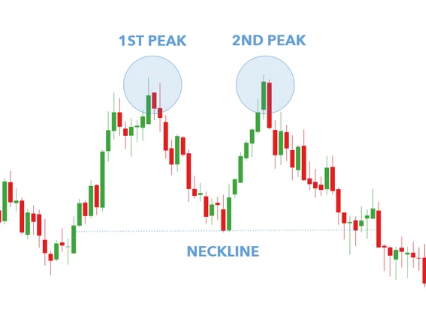

Pattern Double Top – Formasi pergerakan harga yang dikenal sebagai Double Top Pattern adalah formasi yang membentuk dua level tinggi […]

Pattern Double Top – Formasi pergerakan harga yang dikenal sebagai Double Top Pattern adalah formasi yang membentuk dua level tinggi […]